On July 31, 2023, the European Commission adopted the first set of ESRS, abbreviation for European Sustainability Reporting Standards. The ESRS and CSRD herald a new era of corporate transparency and accountability.

In this article, we highlight the key aspects of the first 12 ESRS and answer common questions such as: Which ESRS standards are mandatory, what ESRS disclosures are mandatory, and how do the ESRS relate to other standards? We also shed light on the development, structure and reporting areas of the first set.

Table of Contents

ESRS explained: What are the ESRS standards?

The ESRS standards are reporting standards for sustainability within the EU. The ESRS standards are an integral part of the CSRD, the Corporate Sustainability Reporting Directive of the European Parliament and the Council. This means that the ESRS reporting standards are mandatory. The adoption of the first set of 12 standards by the Commission is considered a significant step to promote sustainable practices and transparency in companies and to contribute to their comparability. This is because the new reporting requirements herald major changes in sustainability reporting and these will affect around 50,000 companies based in the EU. However, subsidiaries, branches abroad and companies that carry out a large part of their business activities in the EU area may also be indirectly affected, which is why the scope of impact can be significantly broader.

Objective of the ESRS and interaction with the EU Green Deal

The ESRS aim to advance the scope and quality of corporate sustainability reporting and promote sustainable development through transparency. Stakeholders, especially investors, other companies and society should gain better insights into the business practices of companies. This is done through various levers.

Overall, sustainability reporting according to ESRS leads to higher quality and comparability of the report contents. However, the impact of the ESRS is not to be limited to their reporting requirements. Companies are also required by ESRS to disclose whether they have improved their sustainability performance and further developed their sustainability management. All of this is intended to accelerate the transformation toward a sustainable economy. The new CSRD standards are thus part of the EU’s master plan to achieve climate neutrality by 2050 and establish a sustainable economic system. Alongside the ESRS and EU Taxonomy Regulation, the Corporate Sustainability Due Diligence Directive and many other EU decisions are important pieces of the puzzle related to the EU Green Deal.

Scope of CSRD and sustainability reporting according to ESRS: Who does ESRS apply to?

- From fiscal year 2024 in the 2025 annual report: Companies that are already subject to a reporting obligation under the NFRD.

- From fiscal year 2025 in the 2026 annual report: All other large corporations with an annual average of 250 employees or more, total assets of 25 million euros or 50 million euros in sales. Two of these three criteria must be met for a company to fall within the scope of the CSRD.

- From fiscal year 2026 in the 2027 annual report: Listed SMEs and small and non-complex credit institutions and captive insurance companies.

- From fiscal year 2028 in the 2029 annual report: Third-country companies with subsidiaries or branches in the EU. This only applies if the threshold of EUR 150 million in net sales in the EU area is exceeded over two years.

The staggered effective date also provides for a transition period (phase-in) for companies before full reporting is required.

ESRS timeline: Milestones for the development of the European reporting standards

The European Commission issues an initial proposal for the CSRD. In addition, the European Financial Reporting Advisory Group (EFRAG) is selected to provide technical advice to the European Commission and to develop the ESRS.

A preliminary political agreement on the CSRD takes place between the Council and the European Parliament.

Public consultation ends and analysis of feedback starts. EFRAG then significantly revises the drafts.

With the ESRS update, a new version of the standards is published and made available to the public on June 9, 2023. The standards have been significantly adapted by the European Commission.

Following the four-week public consultation period, which ended on July 7, 2023, the final delegated regulation supplementing the CSRD is officially adopted on July 31, 2023.

Outlook on ESRS: When will the new standards become legally binding? Before the first set of ESRS reshape the reporting landscape in the EU, they were subject to scrutiny by the European Parliament and the Council. Until Oct 18, 2023, there was a possibility that the EU Parliament would reject the ESRS. However, the objections did not prevail, so the first set of ESRS will enter into force according to plan. Subsequently, the ESRS will be published in the Official Journal.

ESRS summary: How many ESRS are there?

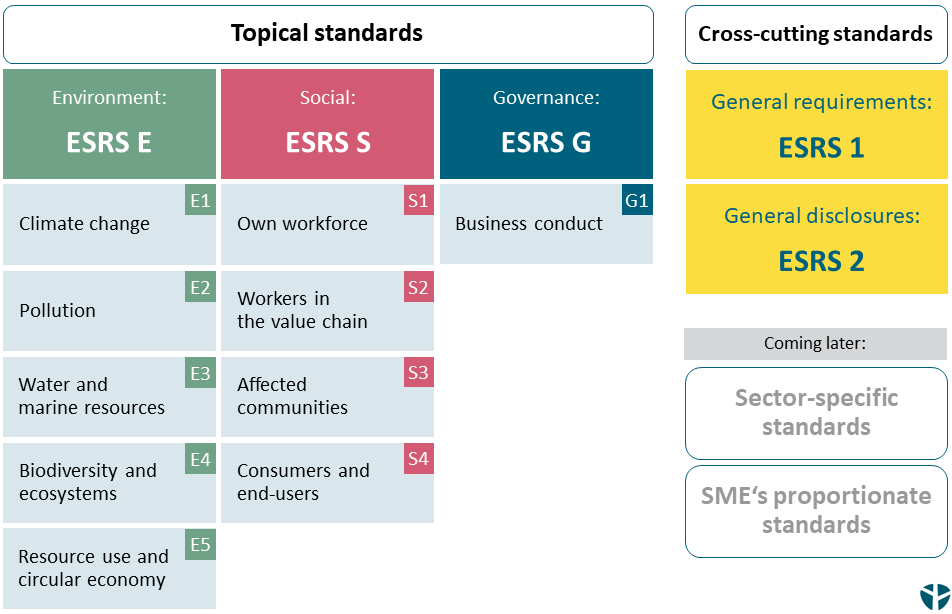

There are 12 ESRS at the current time (as of August 2023). However, more standards are under development and are expected during 2023 and 2024. The so-called first set of ESRS contains two cross-cutting standards and 10 topical standards. The latter each focus on environmental, social and governance topics (ESRS ESG). The new reporting standards enable a simple and logical structure of sustainability information.

Cross-cutting standards ESRS 1 and ESRS 2

Summary ESRS 1 – General requirements:

ESRS 1 contains mandatory principles for the preparation and disclosure of sustainability statements in accordance with the CSRD. ESRS 1 does not contain any specific report content but provides the basis on which reports must be prepared. The standard covers reporting areas, but also specifications on due diligence obligations, the value chain and time specifications, and also defines the way in which sustainability information must be collected and presented. ESRS 1 also requires that the individual standards be subjected to a materiality assessment. ESRS 2 is an exception to this.

The materiality assessment according to ESRS 1 is based on the principle of double materiality. The ESRS materiality assessment thus leans heavily on GRI. It represents a central vehicle of the CSRD for finding out about impacts, risks and opportunities and reporting on them in accordance with the individual ESRS.

The materiality assessment is thus the specified tool for narrowing down the reporting content. Which ESRS and content to report thus depends on what is considered material. However, detailed explanations are required if certain aspects are classified as non-material.

Excursus: What does double materiality mean?

Double materiality means that companies must look at their sustainability aspects from two perspectives. On the one hand, they must consider the impacts of the company according to the inside-out perspective. This dimension is called impact materiality. On the other hand, companies must incorporate financial materiality into the materiality assessment according to the outside-in-perspective.

The principle of double materiality leads companies to address their negative and positive as well as potential and actual impacts on the environment and society. At the same time, the effects of external factors on the company’s own profitability are taken into account.

Summary ESRS 2 – General disclosures:

ESRS 2 specifies general characteristics and information such as policies, measures and objectives that must be reported regardless of the outcome of the materiality assessment. In addition, ESRS 2 specifies the structure and content for the ESRS topical standards. It defines a total of four disclosure areas:

- Governance

- Strategy

- Management of impacts, risks and opportunities

- Metrics and targets

These four pillars are based on TCFD/ISSB and are therefore in line with existing international sustainability reporting frameworks.

ESRS topical standards

The ESRS topics are covered by 10 standards, that take a holistic view of ESG issues. In doing so, they address different ESG reporting content while specifying detailed sustainability information and data.

Summary ESRS E1-E5 – Environmental information:

The five environmental standards cover reporting content on climate change (ESRS E1), pollution (ESRS E2), water and marine resources (ESRS E3), biodiversity and ecosystems (ESRS E4), and resource use and circular economy (ESRS E5). In some cases, they require the company to report on how it is managing the transition to a sustainable business model and has plans in place accordingly. They also include the company’s own contribution to achieving the environmental goals of the EU Green Deal.

Summary ESRS S1-S4 – Social information:

These four standards relate to social aspects and enable companies to report information on their own workforce (ESRS S1) and beyond the company boundary in a structured manner. One of the standards is dedicated to employees in the value chain (ESRS S2). Information on communities affected by the company’s activities (ESRS S3) and consumers and end users (ESRS S4) are also covered by one standard each. The standards ESRS S2-4 do not provide quantitative, but only qualitative information.

Summary ESRS G1 – Governance information:

The governance standard provides a better understanding of a company’s strategy, processes and performance. It includes information on the role of the administrative, performance and supervisory bodies. In addition, the governance standard specifies various reporting contents for the management of impacts, risks and opportunities in the company. Finally, ESRS G1 requires basic information on corporate policy and corporate culture. The standard also provides information on how a company deals with and avoids corruption or bribery and addresses the relationship with suppliers and a company’s political influence.

Outlook for the second set of ESRS: sector-specific standards and ESRS for SMEs

In addition, simplified standards for capital market-oriented small and medium-sized enterprises are expected, the so-called ESRS for SMEs. They address the needs and opportunities of smaller companies and thus contribute to the proportionality of sustainability reporting under ESRS. In addition, voluntary standards are being developed for non-listed SMEs, which are generally not subject to CSRD. The benefit of the ESRS voluntary standards is intended to be that sustainability information can be provided efficiently and proportionately upon request.

Also under development are technical guidelines for implementing machine readability of ESRS statements (XBRL Taxonomy) and specific guidance for supply chain activities and on how to conduct a materiality analysis.

More insights on the ESRS and CSRD

ESRS vs GRI? Overlap with existing frameworks and standards

Large parts of the ESRS metrics, reporting content and procedures are based on already established standards and frameworks. The following examples illustrate this:

- GRI Standards, e.g. for the indicators from the ESRS topical standards and the materiality assessment according to ESRS 1 (ESRS Double Materiality)

- SASB, e.g. for sector-specific standards

- TCFD (Task Force on Climate-Related Financial Disclosures) for addressing climate risks, risk management and financial materiality.

- Science-based Targets and GHG Protocol (Greenhouse Gas Protocol) for dealing with climate strategies.

- CDP (Carbon Disclosure Project) for the calculation of the corporate carbon footprint (Scope-1-2-3) and the financial assessment of opportunities and risks

Companies already working with and familiar with the above standards and frameworks have distinct advantages in ESRS reporting.

ESRS published: In which languages are the ESRS available?

The ESRS are available in 24 languages in total (as of August 2023). The standards are at your disposal as Annex C to the CSRD Delegated Act. All documents and language versions can be viewed on the website of the European Commission and obtained in the download area.

ESRS consultation: What we recommend to companies

The CSRD makes sustainability reporting much more complex. This is because virtually every already known and new sustainability topic is addressed by the ESRS – biodiversity, climate strategies or circular economy, to name just a few examples. In particular, the ESRS Climate Change Standard (ESRS E1) defines high requirements for climate change mitigation measures and climate risk management. In addition, reporting must be in line with the EU Taxonomy Regulation.

We recommend that you use the remaining period for your CSRD compliance. Learn more about how our denkstatt experts can help you on your way to ESRS and CSRD compliance or contact us for ESRS consulting.